Bounce Back

Two Fridays ago, Wall Street got spooked by a poor jobs report. The economy created just 20,000 net new jobs in February while the consensus expected nine times that number. Some are dismissing that as a one-off and not indicative of a souring economy, while others think it is the beginning of more bad news.

A more middling view seems prudent: the economy is still doing well, but not as well. Earnings growth is slowing down. Moreover, we’re currently in the “lull” period between earnings seasons when there’s not a lot of financial or economic news. As such, every news item probably draws undue attention.

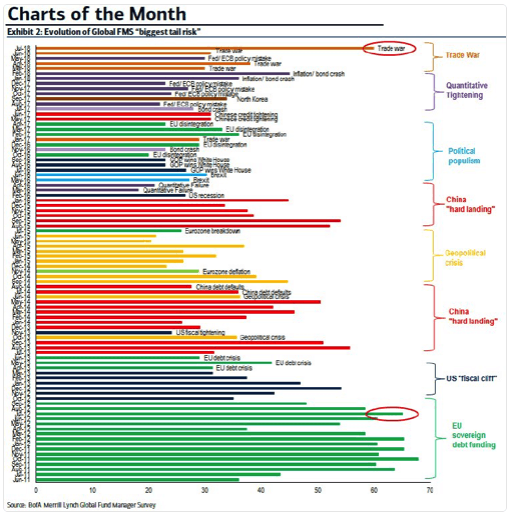

Every day, it seems, the market gets jostled by whatever the current headline is on China, North Korea, or Brexit. These issues simply are not likely to be central to the market’s long-term bearing. For investors (as opposed to traders), everything comes down to earnings and interest rates. Beyond that, the rest is mostly noise.

Domestic stocks posted solid gains last week. The tech sector, the largest segment of the S&P 500, performed best, aided by strength in Apple due to enthusiasm over the expected announcement of a new video streaming service. Industrials lagged, weighed down by a sharp decline in Boeing shares following a second fatal accident involving its new 737 Max 8 airliner. The strong performance of tech shares led to the outperformance of the tech-heavy Nasdaq, which became the strongest major index YTD.

Stocks were strong out of the gate last week, helped by expectations that the U.S. and China would soon reach a trade agreement. Traders seemed particularly encouraged by remarks from the head of China’s central bank at a news conference on Sunday, in which he pledged that China would not devalue its currency to boost exports or to use it as a weapon in trade disputes.

Hopes that a deal was imminent faded as the week progressed, however, after Bloomberg reported that the two countries’ leaders were unlikely to meet until at least early April. Growing concerns over the health of China’s economy may have also caused the midweek stall, but news that Chinese officials were responding with new stimulus seemed to be behind a rally on Friday to close the week.

The week’s domestic economic data continued a recent pattern, with the housing and manufacturing sectors flashing warning signals. New home sales dropped nearly 7 percent in January, well in excess of consensus estimates. Overall industrial production failed to rebound in February as much as hoped, manufacturing output declined for a second straight month, and a gauge of regional factory activity fell more than expected. Core durable goods orders (ex-aircraft and defense) jumped in January by the most in six months, however, raising hopes for a rebound in business investment.

Traders also received some hopeful news about the consumer. January retail sales rose a bit, suggesting that December’s plunge, the worst monthly drop since the financial crisis a decade ago, may have been an aberration. The University of Michigan’s preliminary gauge of March consumer sentiment also rebounded more than expected.

China worries, the mixed U.S. economic signals, and a softer-than-expected inflation reading on Tuesday sent the yield on the benchmark 10-year U.S. Treasury note under 2.60 percent, its lowest level since a brief plunge at the start of January, and closed the week at 2.59 percent.

In Europe, the STOXX Europe 600 moved higher last week, boosted by the declining probability that the UK would leave the EU by the March 29 deadline. The week there was dominated by Brexit politics as UK lawmakers voted on a multiple pieces of legislation ahead of the looming deadline. The FTSE 100 rose after UK Prime Minister Theresa May won parliamentary approval to seek a Brexit delay, while the British pound and the euro also gained against the U.S. dollar.

Chinese stocks also rose last week, buoyed by assurances of economic support from a top official after several indicators underscored the country’s continued slowdown. For the week, the Shanghai Composite rose 1.74 percent and the large-cap CSI 300, considered China’s blue-chip index, added 2.39 percent. Most of the gains came on Friday, when Chinese Premier Li Keqiang said that Beijing was considering cutting some interest rates and banks’ reserve requirements to bolster economic growth. Li also stated that Beijing was keen to help the real economy, particularly small and private businesses, to bolster employment and prevent large layoffs. Elsewhere in Asia, Japan’s Nikkei 225 was up 2 percent.

Other significant news and notes follow:

- British lawmakers voted to postpone the country’s departure from the EU, but narrowly failed to wrest control of the Brexit process from Prime Minister Theresa May’s government. The Brexit endgame (a visual guide). And with time running out until the UK is slated to trigger Article 50 and leave the EU, SEC Chairman Jay Clayton told a group of international bankers last week to brace for price volatility.

- Germany seems headed toward a significant slowdown in growth and perhaps into a recession. Which route the country takes has major implications for Europe and the rest of the world. After recording zero growth in the fourth quarter of 2018, narrowly avoiding back-to-back quarters of economic contraction (the common marker for recessions), one of Germany’s most prestigious research institutes Thursday cut its expectations for German growth this year by almost half.

- “We’ll have news on China. Probably one way or the other, we’re going to know over the next three to four weeks,” President Trump told reporters. He added that China had been “very responsible and very reasonable.” But a final agreement is still far from a sure thing. Treasury Secretary Steven Mnuchin said that a proposed meeting between Mr. Trump and President Xi Jinping of China won’t happen this month because there is still more work to do. Some think it could happen in April.

- Extrapolating if/when the world’s second-biggest economy will overtake the first is a tricky business riddled with caveats.

- The Senate joined the House and voted to overturn the President’s national emergency declaration about the border. As expected, the president vetoed it.

- Despite a campaign promise to end federal debt, President Trump’s budget projects trillion-dollar deficits for the next four years, and no balanced budget for at least 15, despite assuming consistently strong economic growth and no recession going forward.

- President Trump said the Federal Aviation Administration would ground Boeing’s fleet of 737 MAX airliners in a major safety setback for the plane maker after two deadly crashes in less than five months. It was inconvenient for air travelers too.

- President Trump’s former economic adviser, Gary Cohn, speaking on the Freakonomics podcast, said that Mr. Trump’s trade adviser, Peter Navarro, is in his view the only Ph.D.-holding economist in the world who thinks that tariffs do not hurt the economy.

- Friday marked a quarterly collision that traders call “quad witching,” when equity and index futures and options expire. Adding to the fun, dozens of S&P indexes were scheduled to rebalance their holdings at the end of the day. That means ETFs and other index traders will realign their portfolios to match their updated benchmarks, buying shares that have been added and selling stocks that have been dropped. By some estimates, ETFs will need to complete $100 billion in combined buying and selling.

- Economists have lowered their forecasts for U.S. employment and economic growth in the first quarter.

- Howard Marks and Oaktree just waved a big warning flag to credit markets.

- Yale’s asset allocation bears no resemblance to the typical university endowment.

- Envestnet to buy MoneyGuide for $500 million.

- Shake Shack tests four-day work week amid tight U.S. labor market.

- At least 49 people were killed in Christchurch, New Zealand after gunmen opened fire on two mosques. Dozens more are injured, many of them seriously, and the death toll is expected to rise. Three men and one woman have been arrested, with one man, 28, charged with murder. Witnesses say the man strolled in and opened fire on innocent worshipers. Prime Minister Jacinda Ardern said it was a well-coordinated attack and called this “one of New Zealand’s darkest days.” An 87-page manifesto believed to belong to one attacker also has emerged, filled with anti-immigrant and anti-Muslim rhetoric.

- Some states want to require that financial advisors act in clients’ best interests, perhaps clumsily.

- Federal prosecutors are pursuing a criminal investigation into deals Facebook made with “at least two” large smartphone makers to access user data like friend lists and contact information, without explicit consent from its users.

- The bomb cyclone hit hard.

- Peak California.

- Banks and money-laundering.

- Almost 80 investment advisory firms agreed to pay back more than $125 million to clients who were steered into higher-cost mutual funds without being clearly told about cheaper versions.

- Before the 2008 stock market crash, 52 percent of Americans aged 35 or younger were invested in the stock market. As of last year, the number had dropped to 37 percent.

- Consider high-school teacher Donelan Andrews, perhaps the first person ever to read his insurance policy.

[ctct form=”269″]